Since the start of the COVID-19 Pandemic, the automotive industry, specifically new and used retail dealerships, has experienced an uncanny boom in sales revenues and profits.

- The COVID-19 pandemic spurred dramatic declines in the use of public transportation.

- Supply chain issues across the globe caused significant physical inventory shortages.

- Government stimulus released free cash into the economy at never-before-seen levels.

These factors and more combined lead to record-breaking commission checks for the individuals who toughed it out wearing masks to the dealership every day.

A shout-out to America’s car salesman.

But you don’t need to be a Harvard economic scientist to understand that “What goes up, must come down.”

In other words, “mean reversion.” Suggesting, at a minimum, a gradual shift to more “average” historic levels of performance should be expected. A special combination of circumstances drove the boom, and we’d be foolish to think what took place the last few years will continue onward.

Haven’t thought about slower times ahead? Just ask anyone who was working in the dealership following the financial crisis in 2008.

So, if you’re working in sales or sales management at a car dealership, depending on commission checks to pay the bills, what can you do to prepare for a potential “recession” in the automotive industry?

1. Take Inventory

Sound familiar? Taking inventory of your finances means creating a balance sheet and a cash flow statement of your personal money. Make a list of your assets. Make a list of your liabilities (debts). Subtract total liabilities from total assets to get your net worth. Are you positive or negative?

Look at your monthly spending. Do you have any money left over at the end of eacmonth? Are you running your accounts down to zero, or do you have a bunch of cash left over? Not sure where you stand? Take an average of your last six-monthly commission paychecks. Make a list of all your monthly expenses, then add $1-2k per month for all the things you aren’t thinking of, like eating out, concerts, and travel.

Starting with your balance sheet and cash flow will tell you which area(s) need the most attention now.

2. Pay down credit cards, personal loans, and lines of credit.

To best position for success during a slowdown in sales is first, pay off debt with the highest interest rates. Start with credit cards. Watch out for fluctuating interest rates on lines of credit. A Home Equity Line of Credit (HELOC) is on floating rates. This means that every time the Federal Reserve raises interest rates, the interest due on your line of credit goes up. We’ve seen these interest rates go from 2% to 12% over the past year.

A general rule of thumb: Pay off debt on anything that does not increase in value over time.

3. Before Paying Any 0% Loans or Credit Cards – Do these two things first…

Increase your cash reserves by 50%. When you live on commission checks, six months of expenses in an emergency fund is appropriate. Increase this number by 50%.

Life happens. We just don’t know when. Increasing your cash to these levels prevents you from having to take on bad debt when things get tough. Additionally, this puts you in a position to capitalize on opportunities.

Remember, “true wealth is made during the bad times, not the good.”

After increasing cash reserves to the recommended levels, update all insurance policies to account for the rise in home values. Then go pay off your 0% interest credit cards for the new furniture you bought during COVID.

4. Assume Interest Rates Will Be “Higher for Longer”

And don’t expect 2-3% mortgages anytime soon. Preparing to succeed during tough times involves planning for the worst and hoping for the best.

If you’re waiting for interest rates to “come back down,” regardless of your reason, you could be waiting much longer than you ever thought possible. For those lucky enough to buy their first home or investment property in the years leading up to 2022, you were just that, lucky.

According to Trading Economics, the historic average mortgage rate since 1971 is 7.74%!

If you wait around for interest rates to get back down to pre-2022 levels, you may very well miss out on investment opportunities whose growth could far outpace the interest rates today.

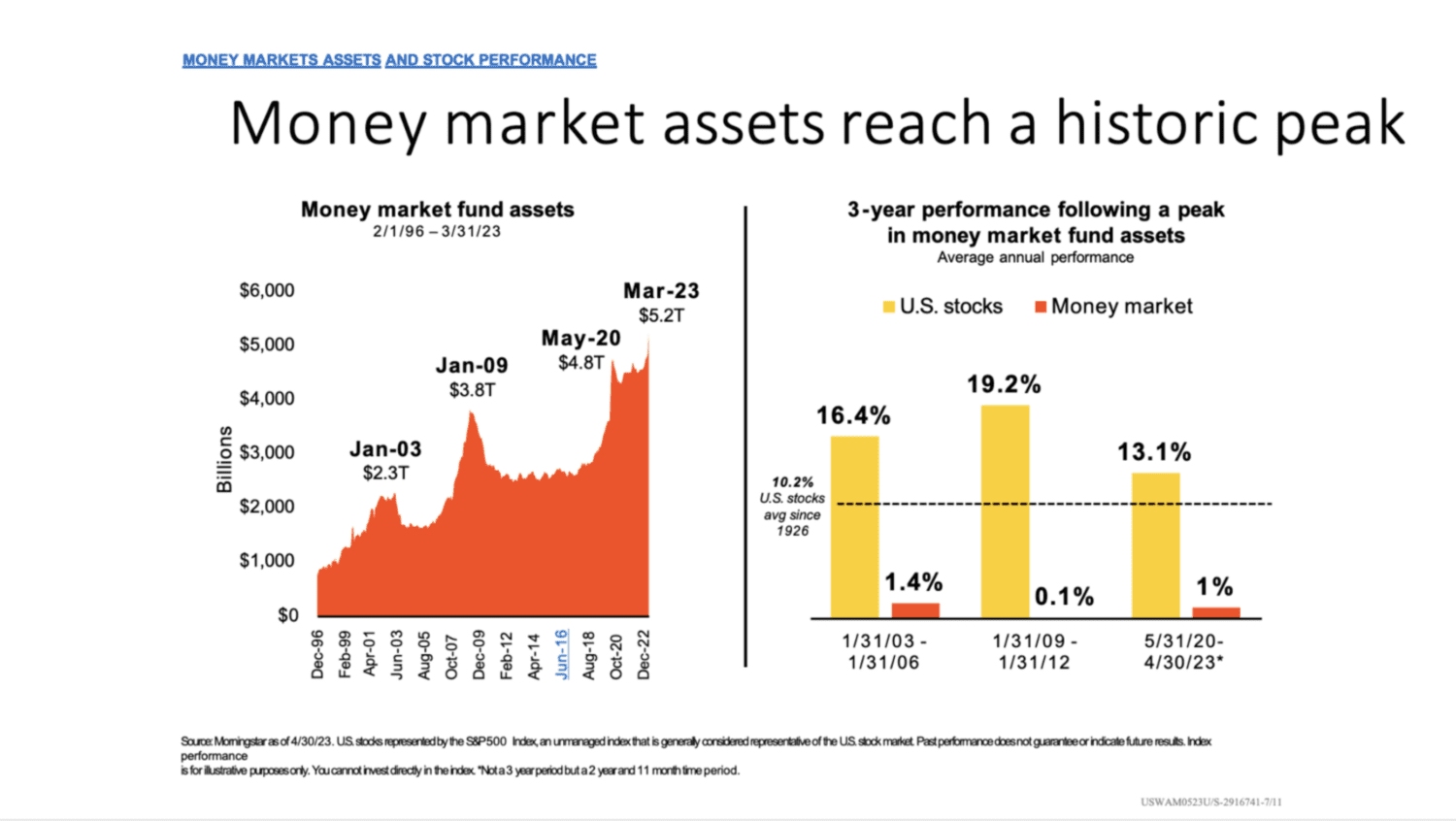

5. Avoid the Money Market Trap

For the first time in over 15 years, money market funds are paying over 5% on cash. Hearing an interest rate like that on money sitting in the bank is pretty good!

Not so fast.

According to Bloomberg, a global financial data company, money market cash has reached a record high of $5.52 Trillion. And while 5% on cash feels great, it won’t help you retire early.

So once you’ve beefed up your cash reserves per the guidelines above, you may want to think twice before putting any more money into your savings account.

Here’s why.

While 5% on cash feels great, how does 15%+ feel? In the three years following the dates, money market funds reached all-time highs; the SP500’s average annual return was 16.4% from 2003 to 2006 and 19.2% from 2009 to 2012. So far, from May 30, 2020, to April 30, 2023, the SP500 has averaged 13.1%. And we just hit another all-time high.