Europe isn’t banning your car.

It’s doing something far more effective.

It’s making sure you can’t realistically keep it.

No politician is standing at a podium announcing a ban on older vehicles. There are no dramatic headlines declaring that your insurance company now controls your transportation. Nobody is openly proposing a system where every aspect of your driving behavior is monitored, scored, and priced in real time. t least not yet.

Instead, something far more subtle is happening.

A new transportation model is emerging, one built on data collection, behavioral monitoring, connected vehicles, digital identity systems, and insurance pricing that increasingly rewards compliance while penalizing deviation. Each piece, viewed independently, sounds reasonable. Put them together, however, and a very different picture begins to emerge.

The automotive industry likes to talk about electric vehicles. Politicians like to talk about emissions. Technology companies like to talk about autonomous driving. But the real battle over the future of transportation isn’t about electric vehicles, self-driving cars, or climate policy. It’s about data. Who collects it. Who owns it. Who profits from it. And ultimately, who uses it to control behavior.

Insurance companies insist they’re simply trying to make roads safer and premiums fairer. That’s the sales pitch behind telematics programs, connected vehicle technology, driver monitoring systems, and usage-based insurance. The more information insurers collect, we’re told, the more accurately they can assess risk. That sounds reasonable.

But there’s a question almost nobody is asking.

When did insurance companies stop measuring risk and start managing behavior?

For decades, insurers looked at a driver’s history, location, age, vehicle type, and claims record. They calculated risk and set a price. Their job wasn’t to influence behavior. Their job was to insure it.

Today, that’s changing.

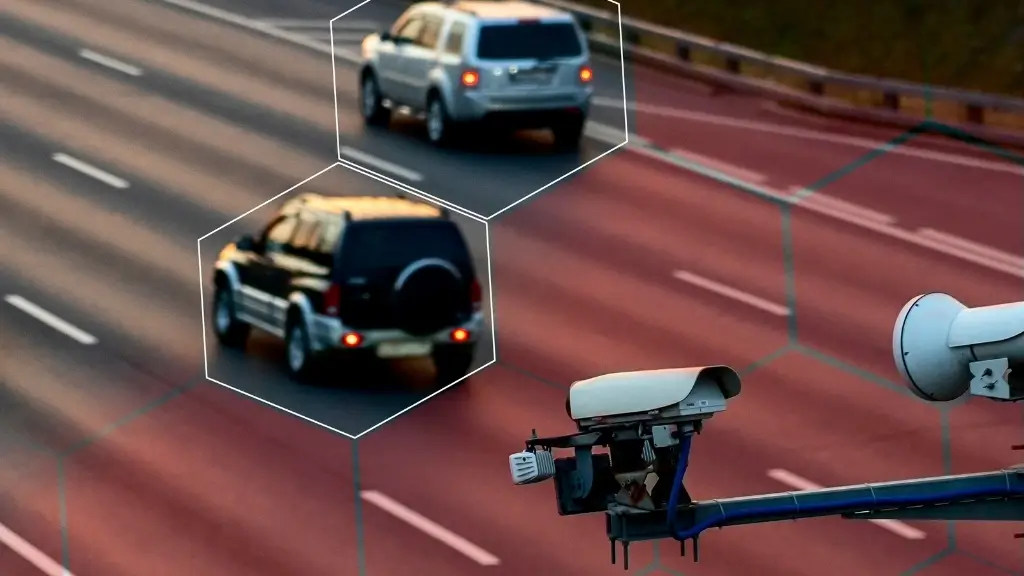

Modern vehicles generate enormous amounts of information. They track speed, location, braking habits, acceleration patterns, mileage, travel times, and in some cases, driver attention. Insurance companies increasingly want access to that data because data is valuable. The more they know about you, the more precisely they can predict your behavior.

And that’s where this story gets interesting.

Because at some point, insurance stops being about risk.

And starts becoming about compliance.

Europe is already providing a glimpse of what that future could look like.

Across the European Union, policymakers, insurers, automakers, and technology providers are building frameworks that connect digital identity, vehicle connectivity, behavioral monitoring, and increasingly sophisticated risk profiling. Industry discussions frequently center around concepts such as the “Transparent Customer,” an idea built around the assumption that more data creates better outcomes.

The name itself sounds harmless.

Who could oppose transparency?

The better question is transparency for whom?

Because transparency is rarely a one-way street.

The vision being discussed isn’t simply about whether you had an accident. It’s about understanding how you live, how you drive, when you drive, where you drive, and potentially much more. Supporters argue that richer data creates fairer pricing. Critics see something different: a system where insurance companies increasingly influence behavior rather than merely insure against risk.

Let me put on my tin-foil hat for a minute.

Maybe I’m completely wrong.

Maybe the rapid expansion of connected vehicles, digital identity systems, usage-based insurance, driver monitoring technology, vehicle data sharing, and behavioral scoring are all unrelated developments moving in completely different directions.

Maybe.

But if they aren’t, where does this road lead?

Imagine a future where insurance pricing is influenced not simply by accidents or tickets, but by a constantly evolving profile built from thousands of data points. Your driving habits. Your travel patterns. Your vehicle usage. Potentially your financial stability. Potentially other lifestyle indicators. Not because a government agency demands it, but because insurers believe more data produces more accurate risk models.

Sound far-fetched?

Ten years ago, most drivers would have considered real-time monitoring of braking, acceleration, mileage, and location data far-fetched too. Today it’s a growing business model. And this is where older vehicles enter the conversation.

Nobody has to ban older cars. That’s the mistake many people make.

Governments don’t necessarily need to outlaw them. Insurance companies don’t need to prohibit them. Cities don’t need to confiscate them.

They simply need to make ownership progressively less practical.

We’ve already seen versions of this play out through low-emission zones, congestion pricing, vehicle restrictions, insurance classifications, and compliance requirements. The vehicle remains legal. You technically still own it. It just becomes increasingly expensive, increasingly inconvenient, and increasingly difficult to use.

That’s how modern control often works.

Not through prohibition.

Through pressure.

Not through confiscation.

Through incentives and penalties.

Not through a dramatic announcement.

Through a thousand small decisions that all move in the same direction.

And that’s why American drivers should pay attention.

Because we’ve seen this movie before.

Europe often moves first. Automakers then adapt globally and that makes the technology spread to regulators and they all follow along.

What begins as a European experiment frequently becomes an American conversation. The future battle over transportation isn’t about electric vehicles.

It’s not about autonomous vehicles.

It’s not even about emissions.

It’s about data.

And the side that controls the data increasingly controls the driver. Keep your ears open for the term “Transparent Customer”, because this is a sign that you don’t want to read.

Check out my full commentary on this story: https://youtu.be/BUlLWw8WAx4

Looking for more automotive news? https://www.CarCoachReports.com

Listen to The Drive Car Show – https://www.youtube.com/@thedrivecarshow