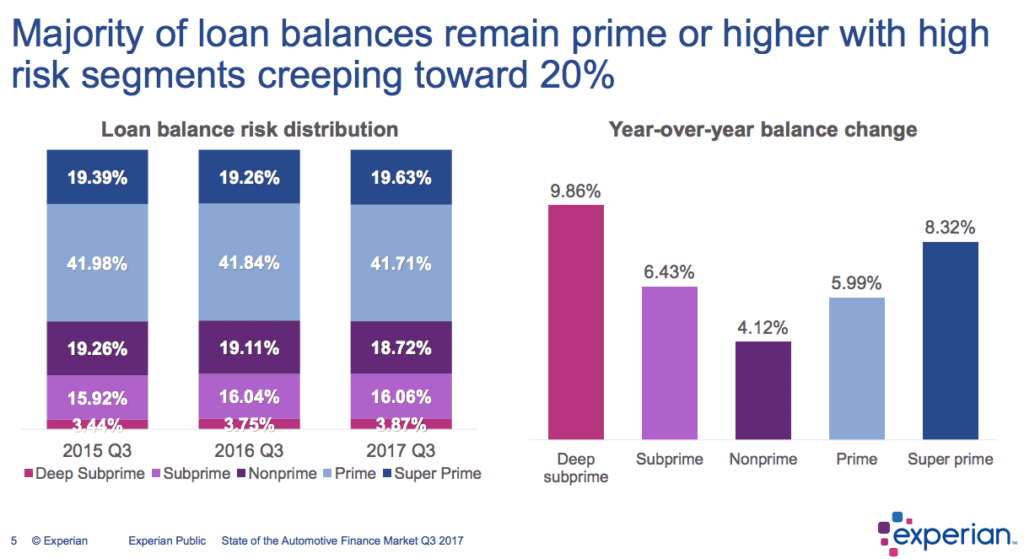

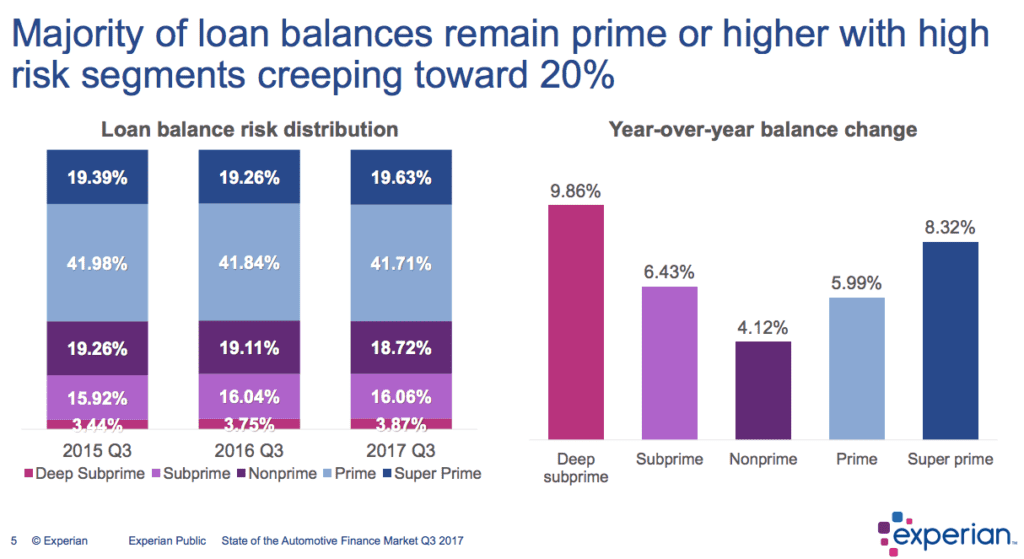

Dec. 07, 2017 — While industry naysayers have predicted the bursting of the so-called auto finance subprime bubble for some time, Experian revealed data that shows that the market continues to gain strength and stability. According to Experian’s latest State of the Automotive Finance Market report, prime consumers grabbed the lion’s share of the total finance market (40.9 percent), while super-prime buyers showed the largest increase, reaching 20.16 percent market share. Conversely, the number of consumers outside prime (with a score of 600 or below) notably decreased, hitting the lowest total auto finance market share on record since 2012.

“The market turning more prime is an encouraging trend. It indicates that industry professionals are using data and analytics as part of the lending process, and consumers are taking a more active role in managing their credit before buying a car,” said Melinda Zabritski, Senior Director of Auto Finance for Experian.

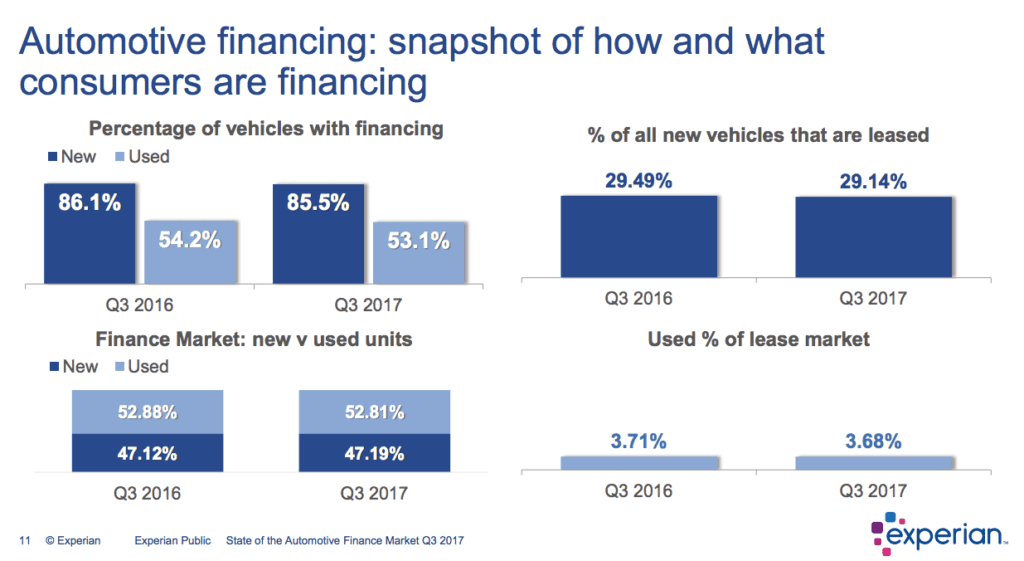

The Q3 report also found that loan terms for new vehicles extended, and credit quality for obtaining a loan on both new and used vehicles notably improved. The average term for new vehicle loans hit an all-time high of 69 months.

Prime and super-prime buyers shifted to used vehicles, growing to make up 49.83 percent of the used car market. In comparison, the percent of buyers outside prime have decreased, making up only 31.34 percent of the market.

“It’s clear that affordability is a driving force in a consumer’s decision to finance a vehicle,” continued Zabritski.

The average amount financed for new vehicles in the third quarter was $30,329, up $291 from Q3 2016. For used vehicles, the average amount financed reached $19,291, an increase of $56 over the previous year. As for monthly payments? For new vehicles, the average payment was $502 per month, increasing by $6 over the previous year, while used vehicle payments averaged $365 per month, up $3 from the previous year.

Other key findings from the Q3 2017 report:

· The average credit score for financing a new vehicle (both loans and leases) was 716.

· The average credit score for financing a used vehicle was 659 (620 for independent and 682 for franchise dealers).

· While average new vehicle loan terms hit 69 months, the average term for used vehicle loans was 64 months.

· Total open automotive loan balances reached $1.121 trillion, up 6.8 percent from the previous year.

· The average new vehicle lease payment was $412, up $6 from Q3 2016.

· The average financing interest rate was 5.1 percent for new vehicles and 8.7 percent for used vehicles.

· Credit unions and captive lenders increased market share of total vehicle financing, growing to 21 percent and 29.8 percent — an increase of 6.9 percent and 35.1 percent, respectively.

· Banks lost market share of total vehicle financing, dropping 6.3 percent to reach 32.9 percent of the market.

For more information regarding this quarter’s analysis, check out Experian’s recorded webinar or go to https://www.experian.com/automotive.

You may also enjoy watching CBT’s interview with Tim Jackson “How to succeed in the current economy, starting with F&I“.